Download the notebook here!

Interactive online version: ![]()

Portfolio optimization: visualization

This notebook visualizes the minimax regret portfolio selection process. It covers:

Conceptual plots explaining regret and confidence penalization

Running the optimizer on a set of investment opportunities

Visualizing selected initiatives and scenario return bands

Imports

[1]:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from impact_engine_allocate.allocation import (

MinimaxRegretAllocation,

calculate_effective_returns,

preprocess,

empty_rule_result,

)

Visualization functions

Helper functions for the four plots used in this tutorial.

[2]:

def plot_regret_concept():

"""Illustrates the concept of regret across different scenarios."""

print("--> Generating plot: Conceptual Example of Regret")

initiatives = {

"A": {"best": 50, "med": 30, "worst": 10},

"B": {"best": 45, "med": 35, "worst": 25},

"C": {"best": 40, "med": 38, "worst": 36},

}

scenarios = ["best", "med", "worst"]

scenario_colors = {"best": "green", "med": "orange", "worst": "red"}

fig, ax = plt.subplots(figsize=(8, 5))

width = 0.2

x = np.arange(len(initiatives))

for i, scenario in enumerate(scenarios):

values = [initiatives[k][scenario] for k in initiatives.keys()]

ax.bar(x + i * width, values, width=width, label=scenario.capitalize(), color=scenario_colors[scenario])

ax.set_xticks(x + width)

ax.set_xticklabels(initiatives.keys())

ax.set_ylabel("Return")

ax.set_title("Conceptual Example of Regret")

ax.legend()

plt.grid(True, axis="y", linestyle="--", alpha=0.6)

plt.tight_layout()

plt.show()

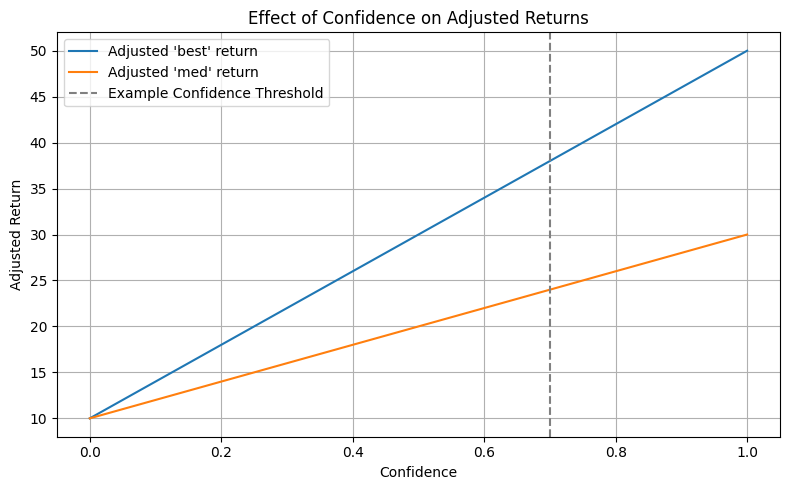

def plot_confidence_penalty_effect():

"""Shows how the effective return is penalized by low confidence."""

print("--> Generating plot: Effect of Confidence on Adjusted Returns")

c = np.linspace(0, 1, 100)

gamma = 1 - c

R_base = {"best": 50, "med": 30, "worst": 10}

plt.figure(figsize=(8, 5))

for scenario in ["best", "med"]:

R_eff = (1 - gamma) * R_base[scenario] + gamma * R_base["worst"]

plt.plot(c, R_eff, label=f"Adjusted '{scenario}' return")

plt.axvline(x=0.7, color="gray", linestyle="--", label="Example Confidence Threshold")

plt.title("Effect of Confidence on Adjusted Returns")

plt.xlabel("Confidence")

plt.ylabel("Adjusted Return")

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

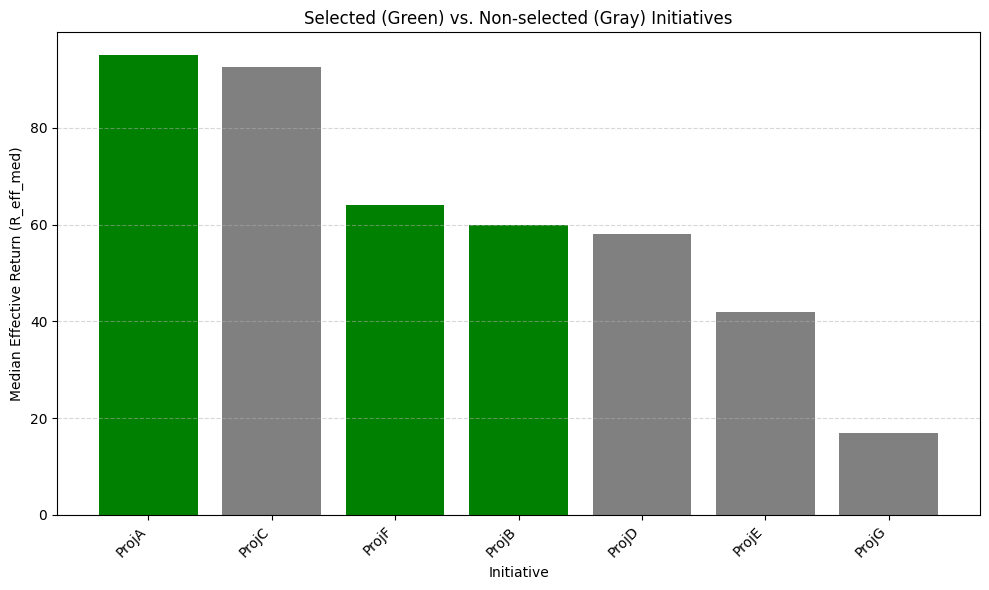

def plot_portfolio_selection(df):

"""Visualizes the selected vs. non-selected initiatives."""

print("--> Generating plot: Selected vs. Non-selected Initiatives")

df_sorted = df.sort_values("R_eff_med", ascending=False)

colors = df_sorted["selected"].map({True: "green", False: "gray"})

plt.figure(figsize=(10, 6))

plt.bar(df_sorted["id"], df_sorted["R_eff_med"], color=colors)

plt.xlabel("Initiative")

plt.ylabel("Median Effective Return (R_eff_med)")

plt.title("Selected (Green) vs. Non-selected (Gray) Initiatives")

plt.xticks(rotation=45, ha="right")

plt.grid(True, axis="y", linestyle="--", alpha=0.5)

plt.tight_layout()

plt.show()

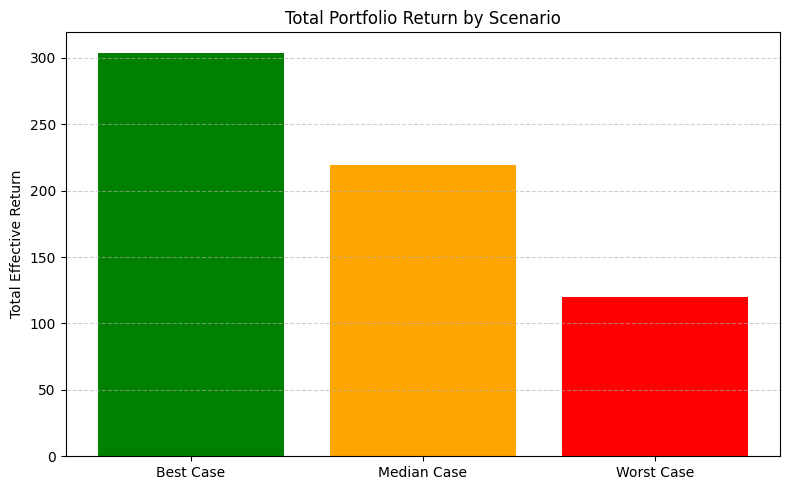

def plot_return_bands(df):

"""Displays the total portfolio return across best, median, and worst-case scenarios."""

print("--> Generating plot: Total Portfolio Return by Scenario")

selected_df = df[df["selected"]]

if selected_df.empty:

print("No initiatives selected, skipping return bands plot.")

return

scenarios = ["R_eff_best", "R_eff_med", "R_eff_worst"]

totals = [selected_df[s].sum() for s in scenarios]

labels = ["Best Case", "Median Case", "Worst Case"]

colors = ["green", "orange", "red"]

plt.figure(figsize=(8, 5))

plt.bar(labels, totals, color=colors)

plt.title("Total Portfolio Return by Scenario")

plt.ylabel("Total Effective Return")

plt.grid(True, axis="y", linestyle="--", alpha=0.6)

plt.tight_layout()

plt.show()

Conceptual plots

Before running the optimizer, we illustrate the two key ideas: regret across scenarios, and how low confidence shrinks effective returns toward the worst case.

[3]:

plot_regret_concept()

plot_confidence_penalty_effect()

--> Generating plot: Conceptual Example of Regret

--> Generating plot: Effect of Confidence on Adjusted Returns

Data and parameters

Define the investment opportunities and optimization constraints.

[4]:

investment_opportunities = [

{"id": "ProjA", "cost": 100, "R_best": 150, "R_med": 100, "R_worst": 50, "confidence": 0.9},

{"id": "ProjB", "cost": 80, "R_best": 120, "R_med": 80, "R_worst": 30, "confidence": 0.6},

{"id": "ProjC", "cost": 120, "R_best": 200, "R_med": 110, "R_worst": 40, "confidence": 0.75},

{"id": "ProjD", "cost": 50, "R_best": 70, "R_med": 60, "R_worst": 20, "confidence": 0.95},

{"id": "ProjE", "cost": 90, "R_best": 160, "R_med": 90, "R_worst": 10, "confidence": 0.4},

{"id": "ProjF", "cost": 60, "R_best": 90, "R_med": 70, "R_worst": 40, "confidence": 0.8},

{"id": "ProjG", "cost": 40, "R_best": 60, "R_med": 30, "R_worst": 10, "confidence": 0.35},

]

BUDGET = 250

CONFIDENCE_THRESHOLD = 0.5

MIN_WORST_RETURN = 80

Run optimization

[5]:

print(f"Parameters: Budget={BUDGET}, Confidence>={CONFIDENCE_THRESHOLD}, Min Worst Return={MIN_WORST_RETURN}")

processed = preprocess(investment_opportunities, CONFIDENCE_THRESHOLD)

if not processed:

results = empty_rule_result("No Eligible Initiatives", "minimax_regret")

else:

solver = MinimaxRegretAllocation()

results = solver(processed, BUDGET, MIN_WORST_RETURN)

print(f"Status: {results['status']}")

if results["status"] == "Optimal":

print(f"Minimized Max Regret: {results['objective_value']:.2f}")

print(f"Selected Initiatives: {results['selected_initiatives']}")

print(f"Total Cost: {results['total_cost']:.2f}")

Parameters: Budget=250, Confidence>=0.5, Min Worst Return=80

Status: Optimal

Minimized Max Regret: 7.50

Selected Initiatives: ['ProjA', 'ProjB', 'ProjF']

Total Cost: 240.00

Visualize results

Build a DataFrame with effective returns and selection flags, then plot the portfolio selection and scenario return bands.

[6]:

if results["status"] == "Optimal":

processed = calculate_effective_returns(investment_opportunities)

initiatives_df = pd.DataFrame(processed)

eff_returns_df = pd.json_normalize(initiatives_df["effective_returns"]).rename(columns=lambda x: f"R_eff_{x}")

initiatives_df = initiatives_df.drop("effective_returns", axis=1).join(eff_returns_df)

initiatives_df["selected"] = initiatives_df["id"].isin(results["selected_initiatives"])

plot_portfolio_selection(initiatives_df)

plot_return_bands(initiatives_df)

else:

print(f"Optimization did not find an optimal solution: {results['status']}")

--> Generating plot: Selected vs. Non-selected Initiatives

--> Generating plot: Total Portfolio Return by Scenario